Recherche avancée

Autres articles (22)

-

Submit enhancements and plugins

13 avril 2011If you have developed a new extension to add one or more useful features to MediaSPIP, let us know and its integration into the core MedisSPIP functionality will be considered.

You can use the development discussion list to request for help with creating a plugin. As MediaSPIP is based on SPIP - or you can use the SPIP discussion list SPIP-Zone. -

D’autres logiciels intéressants

12 avril 2011, parOn ne revendique pas d’être les seuls à faire ce que l’on fait ... et on ne revendique surtout pas d’être les meilleurs non plus ... Ce que l’on fait, on essaie juste de le faire bien, et de mieux en mieux...

La liste suivante correspond à des logiciels qui tendent peu ou prou à faire comme MediaSPIP ou que MediaSPIP tente peu ou prou à faire pareil, peu importe ...

On ne les connais pas, on ne les a pas essayé, mais vous pouvez peut être y jeter un coup d’oeil.

Videopress

Site Internet : (...) -

MediaSPIP Init et Diogène : types de publications de MediaSPIP

11 novembre 2010, parÀ l’installation d’un site MediaSPIP, le plugin MediaSPIP Init réalise certaines opérations dont la principale consiste à créer quatre rubriques principales dans le site et de créer cinq templates de formulaire pour Diogène.

Ces quatre rubriques principales (aussi appelées secteurs) sont : Medias ; Sites ; Editos ; Actualités ;

Pour chacune de ces rubriques est créé un template de formulaire spécifique éponyme. Pour la rubrique "Medias" un second template "catégorie" est créé permettant d’ajouter (...)

Sur d’autres sites (4581)

-

Revision 32858 : on vire ce .foucs() qui "force le scroll" vers l’input du formulaire au ...

12 novembre 2009, par brunobergot@… — Logon vire ce .foucs() qui "force le scroll" vers l’input du formulaire au chargement de la page

-

My SBC Collection

31 décembre 2023, par Multimedia Mike — GeneralLike many computer nerds in the last decade, I have accumulated more than a few single-board computers, or “SBCs”, which are small computers based around a system-on-a-chip (SoC) that nearly always features an ARM CPU at its core. Surprisingly few of these units are Raspberry Pi units, though that brand has come to exemplify and dominate the product category.

Also, as is the case for many computer nerds, most of these SBCs lay fallow for years at a time. Equipped with an inexpensive lightbox that I procured in the last year, I decided I could at least create glamour shots of various units and catalog them in a blog post.

While Raspberry Pi still enjoys the most mindshare far and away, and while I do have a few Raspberry Pi units in my inventory, I have always been a bigger fan of the ODROID brand, which works with convenient importers around the world (in the USA, I can vouch for Ameridroid, to whom I’ve forked over a fair amount of cash for these computing toys).

As mentioned, Raspberry Pi undisputedly has the most mindshare of all these SBC brands and I often wonder why… and then I immediately remind myself that it has the biggest ecosystem, and has a variety of turnkey projects and applications (such as Pi-hole and PiVPN) that promise a lower barrier to entry — as well as a slightly lower price point — than some of these other options. ODROID had a decent ecosystem for awhile, especially considering the monthly ODROID Magazine, though that ceased publication in July 2020. The Raspberry Pi and its variants were famously difficult to come by due to the global chip shortage from 2021-2023. Meanwhile, I had no trouble procuring these boards during the same timeframe.

So let’s delve into the collection…

Cubieboard

The Raspberry Pi came out in 2012 and by 2013 I was somewhat coveting one to hack on. Finally ! An accessible ARM platform to play with. I had heard of the BeagleBoard for years but never tried to get my hands on one. I was thinking about taking the plunge on a new Raspberry Pi, but a colleague told me I should skip that and go with this new hotness called the Cubieboard, based on an Allwinner SoC. The big value-add that this board had vs. a Raspberry Pi was that it had a SATA adapter. Although now that it has been a decade, it only now occurs to me to quander whether it was true SATA or a USB-to-SATA bridge. Looking it up now, I’m led to believe that the SoC supported the functionality natively.Anyway, I did get it up and running but never did much with it, thus setting the tone for future SBC endeavors. No photos because I gave it to another tech enthusiast years ago, whose SBC collection dwarfs my own.

ODROID-XU4

I can’t recall exactly when or how I first encountered the ODROID brand. I probably read about it on some enthusiast page or another circa 2014 and decided to try one out. I eventually acquired a total of 3 of these ODROID-XU4 units, each with a different case, 1 with a fan and 2 passively-cooled :

Collection of ODROID-XU4 SBCs

This is based on the Samsung Exynos 5422 SoC, the same series as was used in their Note 3 phone released in 2013. It has been a fun chip to play with. The XU4 was also my first introduction to the eMMC storage solution that is commonly supported on the ODROID SBCs (alongside micro-SD). eMMC offers many benefits over SD in terms of read/write speed as well as well as longevity/write cycles. That’s getting less relevant these days, however, as more and more SBCs are being released with direct NVMe SSD support.

I had initially wanted to make a retro-gaming device built on this platform (see the handheld section later for more meditations on that). In support of this common hobbyist goal, there is this nifty case XU4 case which apes the aesthetic of the Nintendo N64 :

ODROID-XU4 N64-style case

It even has a cool programmable LCD screen. Maybe one day I’ll find a use for it.

For awhile, one of these XU4 units (likely the noisy, fan-cooled one) was contributing results to the FFmpeg FATE system.

While it features gigabit ethernet and a USB3 port, I once tried to see if I could get 2 Gbps throughput with the unit using a USB3-gigabit dongle. I had curious results in that the total amount of traffic throughput could never exceed 1 Gbps across both interfaces. I.e., if 1 interface was dealing with 1 Gbps and the other interface tried to run at 1 Gbps, they would both only run at 500 Mbps. That remains a mystery to me since I don’t see that limitation with Intel chips.

Still, the XU4 has been useful for a variety of projects and prototyping over the years.

ODROID-HC2 NAS

I find that a lot of my fellow nerds massively overengineer their homelab NAS setups. I’ll explore this in a future post. For my part, people tend to find my homelab NAS solution slightly underengineered. This is the ODROID-HC2 (the “HC” stands for “Home Cloud”) :

ODROID-HC2 NAS

It has the same guts as the ODROID-XU4 except no video output and the USB3 function is leveraged for a SATA bridge. This allows you to plug a SATA hard drive directly into the unit :

ODROID-HC2 NAS uncovered

Believe it or not, this has been my home NAS solution for something like 6 or 7 years now– I don’t clearly remember when I purchased it and put it into service.

But isn’t this sort of irresponsible ? What about a failure of the main drive ? That’s why I have an external drive connected for backing up the most important data via rsync :

ODROID-HC2 NAS backup enclosure

The power consumption can’t be beat– Profiling for a few weeks of average usage worked out to 4.5 kWh for the ODROID-HC2… per month.

ODROID-C2

I was on a kick of ordering more SBCs at one point. This is the ODROID-C2, equipped with a 64-bit Amlogic SoC :

ODROID-C2

I had this on the FATE farm for awhile, performing 64-bit ARM builds (vs. the XU4’s 32-bit builds). As memory serves, it was unreliable and would occasionally freeze up.

Here is a view of the eMMC storage through the bottom of the translucent case :

Bottom of ODROID-C2 with view of eMMC storage

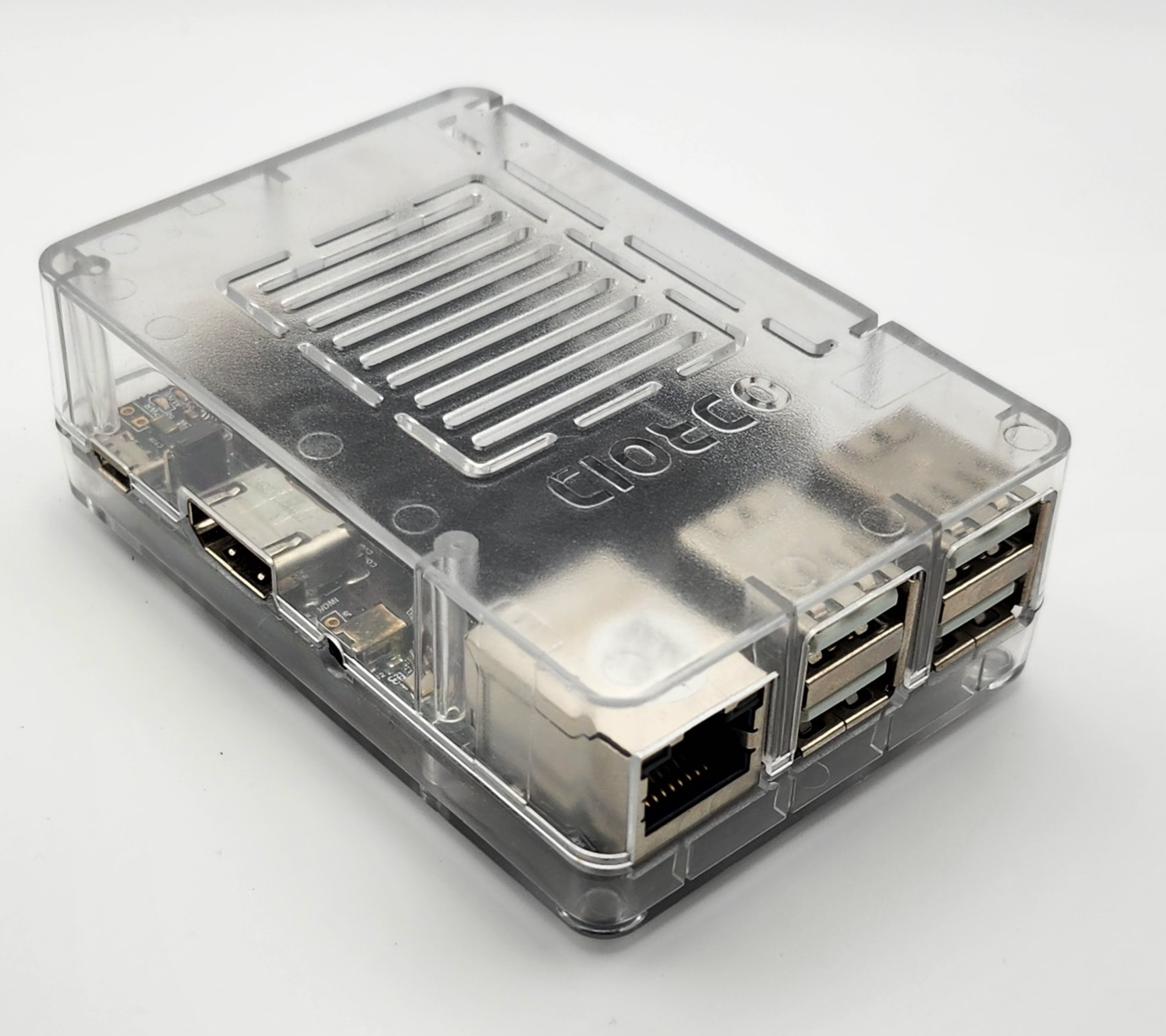

ODROID-N2+

Out of all my ODROID SBCs, this is the unit that I long to “get back to” the most– the ODROID-N2+ :

ODROID-N2+

Very capable unit that makes a great little desktop. I have some projects I want to develop using it so that it will force me to have a focused development environment.

Raspberry Pi

Eventually, I did break down and get a Raspberry Pi. I had a specific purpose in mind and, much to my surprise, I have stuck to it :

Original Raspberry Pi

I was using one of the ODROID-XU4 units as a VPN gateway. Eventually, I wanted to convert the XU4 to something else and I decided to run the VPN gateway as an appliance on the simplest device I could. So I procured this complete hand-me-down unit from eBay and went to work. This was also the first time I discovered the DietPi distribution and this box has been in service running Wireguard via PiVPN for many years.

I also have a Raspberry Pi 3B+ kicking around somewhere. I used it as a Steam Link device for awhile.

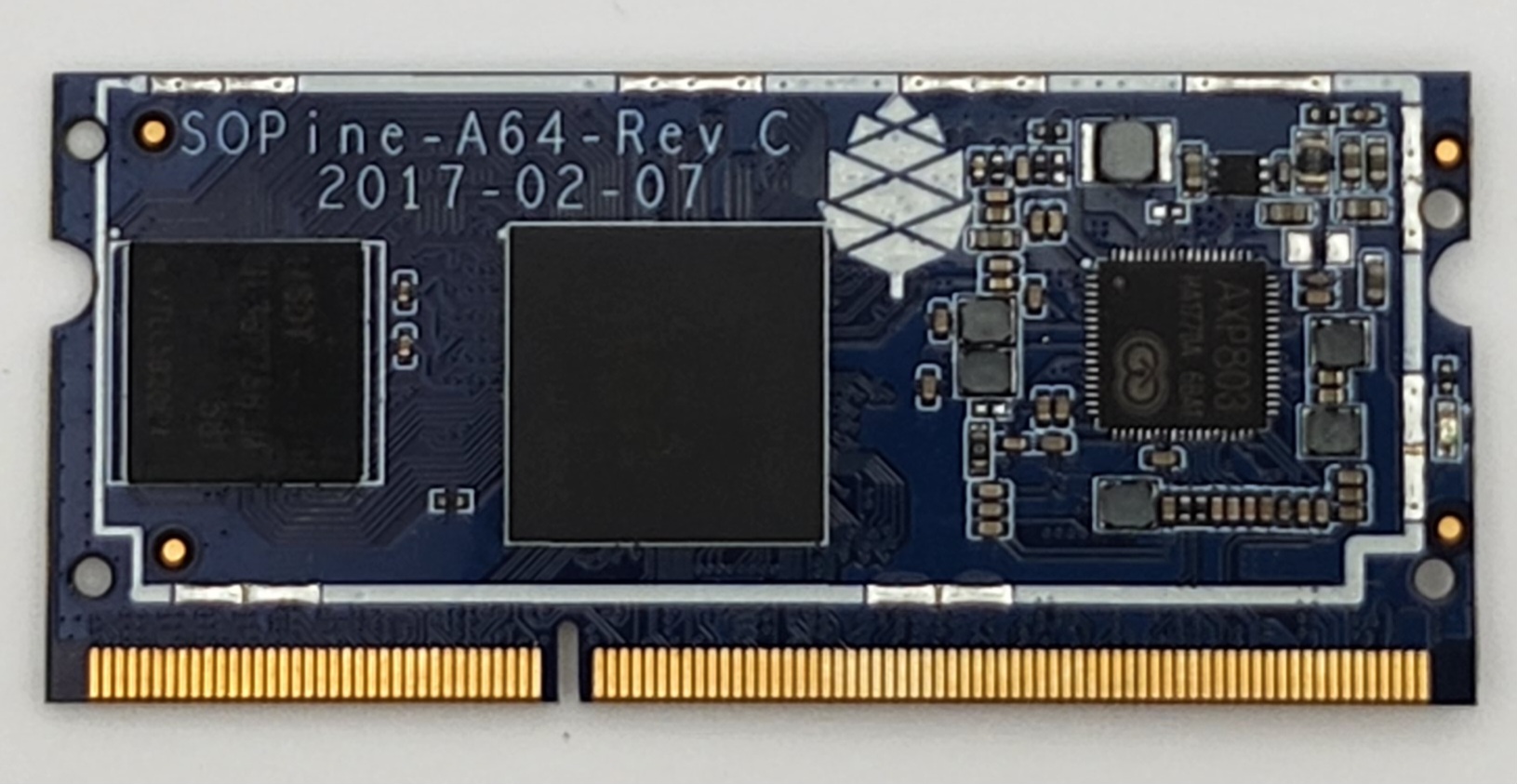

SOPINE + Baseboard

Also procured when I was on this “let’s buy random SBCs” kick. The Pine64 SOPINE is actually a compute module that comes in the form factor of a memory module.

Pine64 SOPINE Compute Module

Back to using Allwinner SoCs. In order to make this thing useful, you need to place it in something. It’s possible to get a mini-ITX form factor board that can accommodate 7 of these modules. Before going to that extreme, there is this much simpler baseboard which can also use eMMC for storage.

Baseboard with SOPINE, eMMC, and heat sinks

I really need to find an appropriate case for this one as it currently performs its duty while sitting on an anti-static bag.

NanoPi NEO3

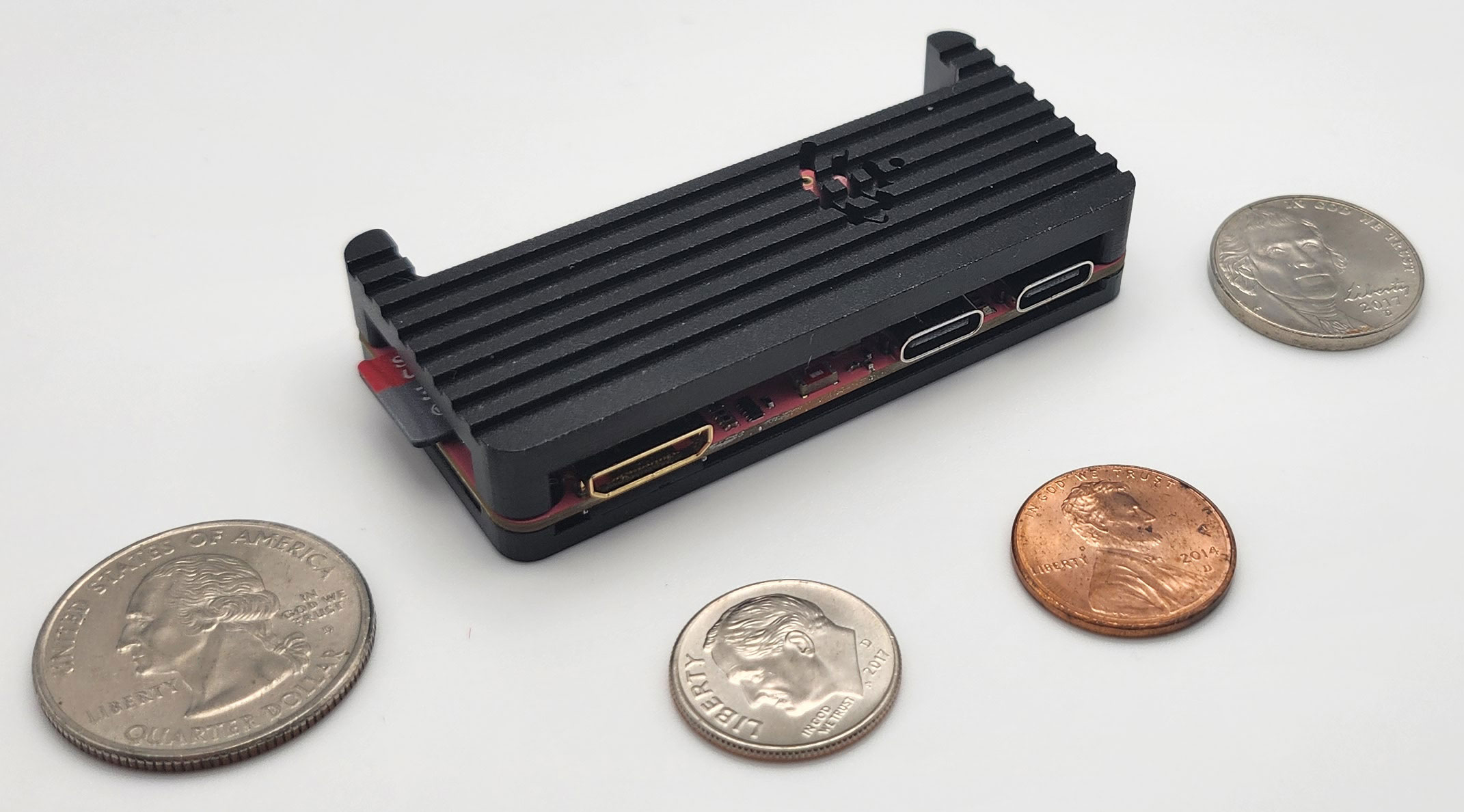

I enjoy running the DietPi distribution on many of these SBCs (as it’s developed not just for Raspberry Pi). I have also found their website to be a useful resource for discovering new SBCs. That’s how I found the NanoPi series and zeroed in on this NEO3 unit, sporting a Rockchip SoC, and photographed here with some American currency in order to illustrate its relative size :

NanoPi NEO3

I often forget about this computer because it’s off in another room, just quietly performing its assigned duty.

MangoPi MQ-Pro

So far, I’ve heard of these fruits prepending the Greek letter pi for naming small computing products :- Raspberry – the O.G.

- Banana – seems to be popular for hobbyist router/switches

- Orange

- Atomic

- Nano

- Mango

Okay, so the AtomicPi and NanoPi names don’t really make sense considering the fruit convention.

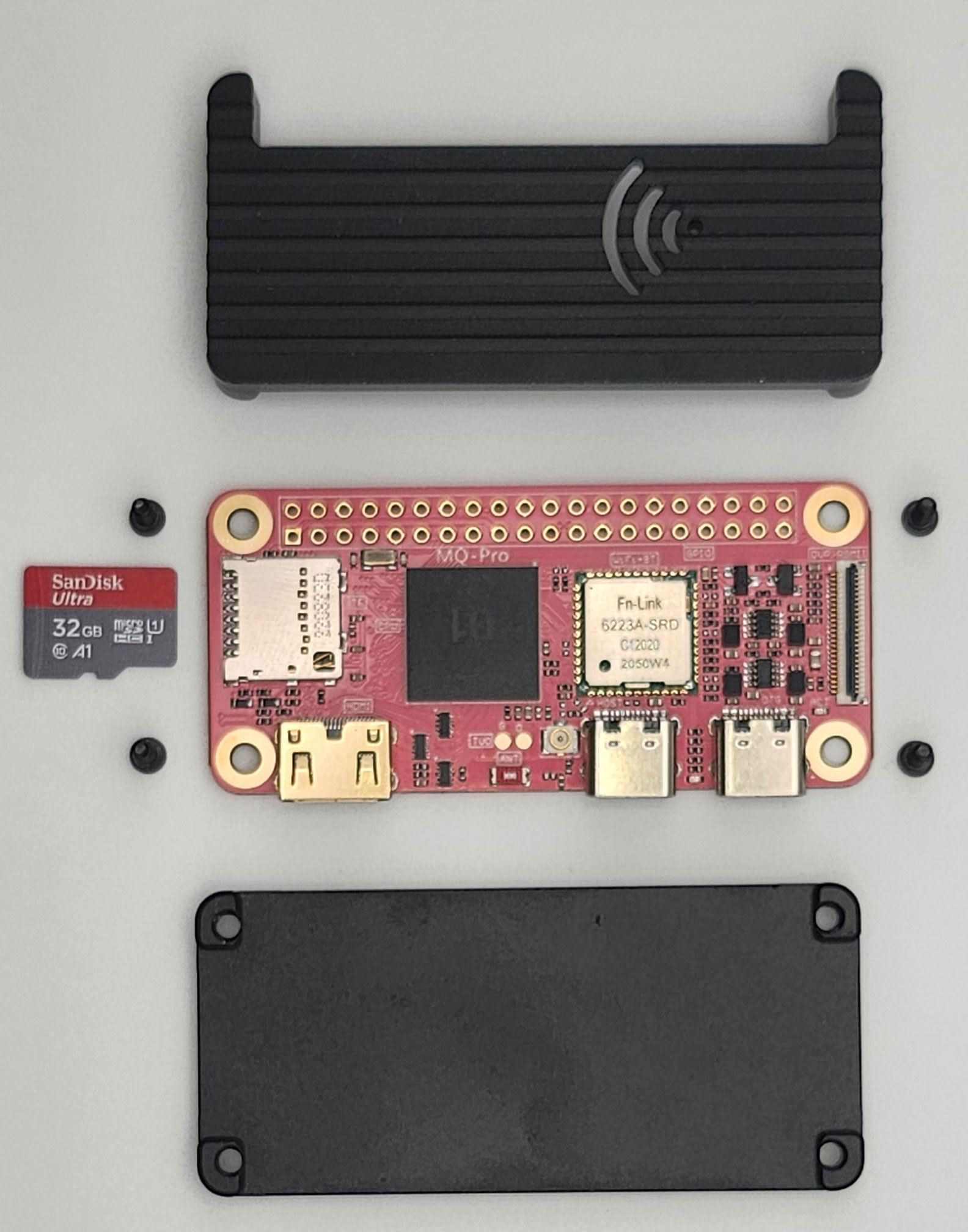

Anyway, the newest entry is the MangoPi. These showed up on Ameridroid a few months ago. There are 2 variants : the MQ-Pro and the MQ-Quad. I picked one and rolled with it.

MangoPi MQ-Pro pieces arrive

When it arrived, I unpacked it, assembled the pieces, downloaded a distro, tossed that on a micro-SD card, connected a monitor and keyboard to it via its USB-C port, got the distro up and running, configured the wireless networking with a static IP address and installed sshd, and it was ready to go as a headless server for an edge application.

MangoPi MQ-Pro components, ready for assembly

The unit came with no instructions that I can recall. After I got it set up, I remember thinking, “What is wrong with me ? Why is it that I just know how to do all of this without any documentation ?”

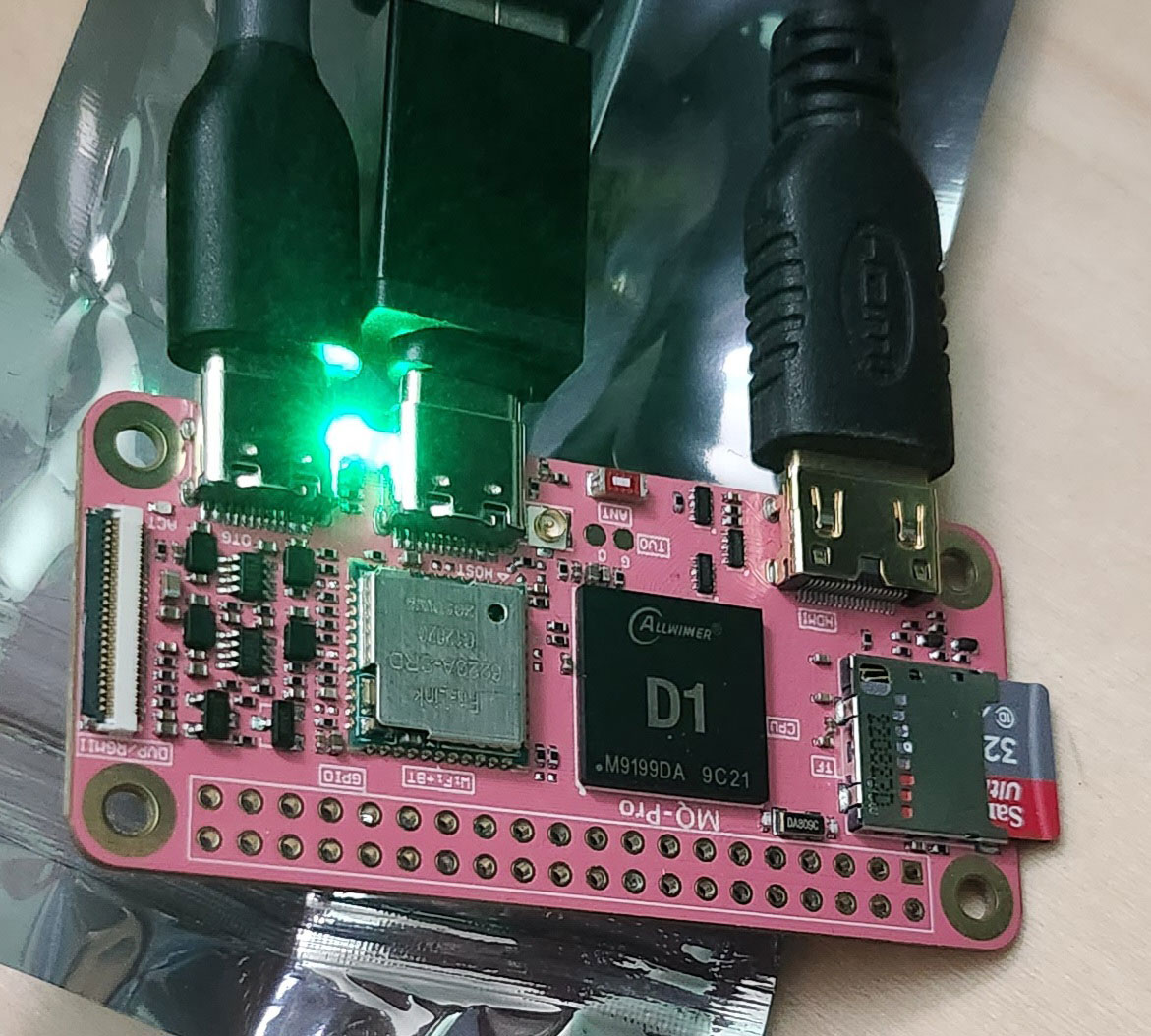

MangoPi MQ-Pro in first test

Only after I got it up and running and poked around a bit did I realize that this SBC doesn’t have an ARM SoC– it’s a RISC-V SoC. It uses the Allwinner D1, so it looks like I came full circle back to Allwinner.

MangoPi MQ-Pro with more US coinage for scale

So I now have my first piece of RISC-V hobbyist kit, although I learned recently from Kostya that it’s not that great for multimedia.

Handheld Gaming Units

The folks at Hardkernel have also produced a series of handheld retro-gaming devices called ODROID-GO. The first one resembled the original Nintendo Game Boy, came as a kit to be assembled, and emulated 5 classic consoles. It also had some hackability to it. Quite a cool little device, and inexpensive too. I have since passed it along to another gaming enthusiast.Later came the ODROID-GO Advance, also a kit, but emulating more devices. I was extremely eager to get my hands on this since it could emulate SNES in addition to NES. It also features a headphone jack, unlike the earlier model. True to form, after I received mine, it took me about 13 months before I got around to assembling it. After that, the biggest challenge I had was trying to find an appropriate case for it.

ODROID-GO Advance with case and headphones

Even though it may try to copy the general aesthetic and form factor of the Game Boy Advance, cases for the GBA don’t fit this correctly.

Further, Hardkernel have also released the ODROID-GO Super and Ultra models that do more and more. The Advance, Super, and Ultra models have powerful SoCs and feature much more hackability than the first ODROID-GO model.

I know that the guts of the Advance have been used in other products as well. The same is likely true for the Super and Ultra.

Ultimately, the ODROID-GO Advance was just another project I assembled and then set aside since I like the idea of playing old games much more than actually doing it. Plus, the fact has finally crystalized in my mind over the past few years that I have never enjoyed handheld gaming and likely will never enjoy handheld gaming, even after I started wearing glasses. Not that I’m averse to old Game Boy / Color / Advance games, but if I’m going to play them, I’d rather emulate them on a large display.

The Future

In some of my weaker moments, I consider ordering up certain Banana Pi products (like the Banana Pi BPI-R2) with a case and doing my own router tricks using some open source router/firewall solution. And then I remind myself that my existing prosumer-type home router is doing just fine. But maybe one day…The post My SBC Collection first appeared on Breaking Eggs And Making Omelettes.

-

Adventures In NAS

1er janvier, par Multimedia Mike — GeneralIn my post last year about my out-of-control single-board computer (SBC) collection which included my meager network attached storage (NAS) solution, I noted that :

I find that a lot of my fellow nerds massively overengineer their homelab NAS setups. I’ll explore this in a future post. For my part, people tend to find my homelab NAS solution slightly underengineered.

So here I am, exploring this is a future post. I’ve been in the home NAS game a long time, but have never had very elaborate solutions for such. For my part, I tend to take an obsessively reductionist view of what constitutes a NAS : Any small computer with a pool of storage and a network connection, running the Linux operating system and the Samba file sharing service.

Many home users prefer to buy turnkey boxes, usually that allow you to install hard drives yourself, and then configure the box and its services with a friendly UI. My fellow weird computer nerds often buy cast-off enterprise hardware and set up more resilient, over-engineered solutions, as long as they have strategies to mitigate the noise and dissipate the heat, and don’t mind the electricity bills.

If it works, awesome ! As an old hand at this, I am rather stuck in my ways, however, preferring to do my own stunts, both with the hardware and software solutions.

My History With Home NAS Setups

In 1998, I bought myself a new computer — beige box tower PC, as was the style as the time. This was when normal people only had one computer at most. It ran Windows, but I was curious about this new thing called “Linux” and learned to dual boot that. Later that year, it dawned on me that nothing prevented me from buying a second ugly beige box PC and running Linux exclusively on it. Further, it could be a headless Linux box, connected by ethernet, and I could consolidate files into a single place using this file sharing software named Samba.

I remember it being fairly onerous to get Samba working in those days. And the internet was not quite so helpful in those days. I recall that the thing that blocked me for awhile was needing to know that I had to specify an entry for the Samba server machine in the LMHOSTS (Lanman hosts) file on the Windows 95 machine.

However, after I cracked that code, I have pretty much always had some kind of ad-hoc home NAS setup, often combined with a headless Linux development box.

In the early 2000s, I built a new beige box PC for a file server, with a new hard disk, and a coworker tutored me on setting up a (P)ATA UDMA 133 (or was it 150 ? anyway, it was (P)ATA’s last hurrah before SATA conquered all) expansion card and I remember profiling that the attached hard drive worked at a full 21 MBytes/s reading. It was pretty slick. Except I hadn’t really thought things through. You see, I had a hand-me-down ethernet hub cast-off from my job at the time which I wanted to use. It was a 100 Mbps repeater hub, not a switch, so the catch was that all connected machines had to be capable of 100 Mbps. So, after getting all of my machines (3 at the time) upgraded to support 10/100 ethernet (the old off-brand PowerPC running Linux was the biggest challenge), I profiled transfers and realized that the best this repeater hub could achieve was about 3.6 MBytes/s. For a long time after that, I just assumed that was the upper limit of what a 100 Mbps network could achieve. Obviously, I now know that the upper limit ought to be around 11.2 MBytes/s and if I had gamed out that fact in advance, I would have realized it didn’t make sense to care about super-fast (for the time) disk performance.

At this time, I was doing a lot for development for MPlayer/xine/FFmpeg. I stored all of my multimedia material on this NAS. I remember being confused when I was working with Y4M data, which is raw frames, which is lots of data. xine, which employed a pre-buffering strategy, would play fine for a few seconds and then stutter. Eventually, I reasoned out that the files I was working with had a data rate about twice what my awful repeater hub supported, which is probably the first time I came to really understand and respect streaming speeds and their implications for multimedia playback.

Smaller Solutions

For a period, I didn’t have a NAS. Then I got an Apple AirPort Extreme, which I noticed had a USB port. So I bought a dual drive brick to plug into it and used that for a time. Later (2009), I had this thing called the MSI Wind Nettop which is the only PC I’ve ever seen that can use a CompactFlash (CF) card for a boot drive. So I did just that, and installed a large drive so it could function as a NAS, as well as a headless dev box. I’m still amazed at what a low-power I/O beast this thing is, at least when compared to all the ARM SoCs I have tried in the intervening 1.5 decades. I’ve had spinning hard drives in this thing that could read at 160 MBytes/s (‘dd’ method) and have no trouble saturating the gigabit link at 112 MBytes/s, all with its early Intel Atom CPU.Around 2015, I wanted a more capable headless dev box and discovered Intel’s line of NUCs. I got one of the fat models that can hold a conventional 2.5″ spinning drive in addition to the M.2 SATA SSD and I was off and running. That served me fine for a few years, until I got into the ARM SBC scene. One major limitation here is that 2.5″ drives aren’t available in nearly the capacities that make a NAS solution attractive.

Current Solution

My current NAS solution, chronicled in my last SBC post– the ODroid-HC2, which is a highly compact ARM SoC with an integrated USB3-SATA bridge so that a SATA drive can be connected directly to it :

ODROID-HC2 NAS

I tend to be weirdly proficient at recalling dates, so I’m surprised that I can’t recall when I ordered this and put it into service. But I’m pretty sure it was circa 2018. It’s only equipped with an 8 TB drive now, but I seem to recall that it started out with only a 4 TB drive. I think I upgraded to the 8 TB drive early in the pandemic in 2020, when ISPs were implementing temporary data cap amnesty and I was doing what a r/DataHoarder does.

The HC2 has served me well, even though it has a number of shortcomings for a hardware set chartered for NAS :

- While it has a gigabit ethernet port, it’s documented that it never really exceeds about 70 MBytes/s, due to the SoC’s limitations

- The specific ARM chip (Samsung Exynos 5422 ; more than a decade old as of this writing) lacks cryptography instructions, slowing down encryption if that’s your thing (e.g., LUKS)

- While the SoC supports USB3, that block is tied up for the SATA interface ; the remaining USB port is only capable of USB2 speeds

- 32-bit ARM, which prevented me from running certain bits of software I wanted to try (like Minio)

- Only 1 drive, so no possibility for RAID (again, if that’s your thing)

I also love to brag on the HC2’s power usage : I once profiled the unit for a month using a Kill-A-Watt and under normal usage (with the drive spinning only when in active use). The unit consumed 4.5 kWh… in an entire month.

New Solution

Enter the ODroid-HC4 (I purchased mine from Ameridroid but Hardkernel works with numerous distributors) :

ODroid-HC4 with an SSD and a conventional drive

I ordered this earlier in the year and after many months of procrastinating and obsessing over the best approach to take with its general usage, I finally have it in service as my new NAS. Comparing point by point with the HC2 :

- The gigabit ethernet runs at full speed (though a few things on my network run at 2.5 GbE now, so I guess I’ll always be behind)

- The ARM chip (Amlogic S905X3) has AES cryptography acceleration and handles all the LUKS stuff without breaking a sweat ; “cryptsetup benchmark” reports between 500-600 MBytes/s on all the AES variants

- The USB port is still only USB2, so no improvement there

- 64-bit ARM, which means I can run Minio to simulate block storage in a local dev environment for some larger projects I would like to undertake

- Supports 2 drives, if RAID is your thing

How I Set It Up

How to set up the drive configuration ? As should be apparent from the photo above, I elected for an SSD (500 GB) for speed, paired with a conventional spinning HDD (18 TB) for sheer capacity. I’m not particularly trusting of RAID. I’ve watched it fail too many times, on systems that I don’t even manage, not to mention that aforementioned RAID brick that I had attached to the Apple AirPort Extreme.I had long been planning to use bcache, the block caching interface for Linux, which can use the SSD as a speedy cache in front of the more capacious disk. There is also LVM cache, which is supposed to achieve something similar. And then I had to evaluate the trade-offs in whether I wanted write-back, write-through, or write-around configurations.

This was all predicated on the assumption that the spinning drive would not be able to saturate the gigabit connection. When I got around to setting up the hardware and trying some basic tests, I found that the conventional HDD had no trouble keeping up with the gigabit data rate, both reading and writing, somewhat obviating the need for SSD acceleration using any elaborate caching mechanisms.

Maybe that’s because I sprung for the WD Red Pro series this time, rather than the Red Plus ? I’m guessing that conventional drives do deteriorate over the years. I’ll find out.

For the operating system, I stuck with my newest favorite Linux distro : DietPi. While HardKernel (parent of ODroid) makes images for the HC units, I had also used DietPi for the HC2 for the past few years, as it tends to stay more up to date.

Then I rsync’d my data from HC2 -> HC4. It was only about 6.5 TB of total data but it took days as this WD Red Plus drive is only capable of reading at around 10 MBytes/s these days. Painful.

For file sharing, I’m pretty sure most normal folks have nice web UIs in their NAS boxes which allow them to easily configure and monitor the shares. I know there are such applications I could set up. But I’ve been doing this so long, I just do a bare bones setup through the terminal. I installed regular Samba and then brought over my smb.conf file from the HC2. 1 by 1, I tested that each of the old shares were activated on the new NAS and deactivated on the old NAS. I also set up a new share for the SSD. I guess that will just serve as a fast I/O scratch space on the NAS.

The conventional drive spins up and down. That’s annoying when I’m actively working on something but manage not to hit the drive for like 5 minutes and then an application blocks while the drive wakes up. I suppose I could set it up so that it is always running. However, I micro-manage this with a custom bash script I wrote a long time ago which logs into the NAS and runs the “date” command every 2 minutes, appending the output to a file. As a bonus, it also prints data rate up/down stats every 5 seconds. The spinning file (“nas-main/zz-keep-spinning/keep-spinning.txt”) has never been cleared and has nearly a quarter million lines. I suppose that implies that it has kept the drive spinning for 1/2 million minutes which works out to around 347 total days. I should compare that against the drive’s SMART stats, if I can remember how. The earliest timestamp in the file is from March 2018, so I know the HC2 NAS has been in service at least that long.

For tasks, vintage cron still does everything I could need. In this case, that means reaching out to websites (like this one) and automatically backing up static files.

I also have to have a special script for starting up. Fortunately, I was able to bring this over from the HC2 and tweak it. The data disks (though not boot disk) are encrypted. Those need to be unlocked and only then is it safe for the Samba and Minio services to start up. So one script does all that heavy lifting in the rare case of a reboot (this is the type of system that’s well worth having on a reliable UPS).

Further Work

I need to figure out how to use the OLED display on the NAS, and how to make it show something more useful than the current time and date, which is what it does in its default configuration with HardKernel’s own Linux distro. With DietPi, it does nothing by default. I’m thinking it should be able to show the percent usage of each of the 2 drives, at a minimum.I also need to establish a more responsible backup regimen. I’m way too lazy about this. Fortunately, I reason that I can keep the original HC2 in service, repurposed to accept backups from the main NAS. Again, I’m sort of micro-managing this since a huge amount of data isn’t worth backing up (remember the whole DataHoarder bit), but the most important stuff will be shipped off.

The post Adventures In NAS first appeared on Breaking Eggs And Making Omelettes.